2 / 3

2 / 3

Email your feedback and queries

to:

propertyqs@thesundaily.comX

ON FRIDAY

DECEMBER 12, 2014

W

HAT

is themeaning of the

word “affordability”?

According to a business

dictionary, it is

a conclusion

drawn from the analysis of the life

cycle cost of a proposed acquisition;

that the purchase is in accordwith the

resources and long-termrequirements

of the acquirer

. A shorter and simpler

explanationwould be

one’s financial

means in relation to a purchase

.

CONTEXT AND CIRCUMSTANCE

With that, we probe a little further,

questioning one’s financial means where

house purchase is concerned. Is the

average income earner able to purchase a

roof over his head and live reasonably

comfortably today? Howmuch would he

or she need to earn? And if good

employment and better salaries are found

in the main cities and big towns, are there

affordable houses readily available in these

urban areas? What kind of price tags do

affordable houses come with? How

affordable is affordable? Ultimately, the big

question is, is there an issue where housing

affordability is concerned?

To answer all this is Dr Yeah KimLeng,

dean of the School of Business at theMalaysia

University of Science and Technology

(MUST). Yeah has aMasters in Business

Administration and holds a PhD in

Agricultural and Resource Economics,

specialising in development economics. He

was previously the group chief economist of a

local rating agency andmanaging director for

its research and consultancy firm. Prior to

that, he held the post of senior analyst at the

Institute of Strategic and International

StudiesMalaysia where he was involved in

research on various national economic

policies.

According toYeah,

housing affordability

is a complex socio-economic issuewith

important political implications

. “First, let

me explainwhat housing affordability is. It is

basically the ability or inability to own a

house or have a permanent roof over one’s

head,” he says. With that, we ask then, howdo

we knowwhen housing affordability becomes

amajor concern. “At the national level, we

track overall affordability in several ways.

One index compares house price increases

with income increases. If the ratio is below

one, then the rise in income has not kept pace

Housing

affordability

> Issues, effects and

areas toexamine

with house price increases, indicating a

decline in housing affordability. We can track

this by state and by housing segment.”

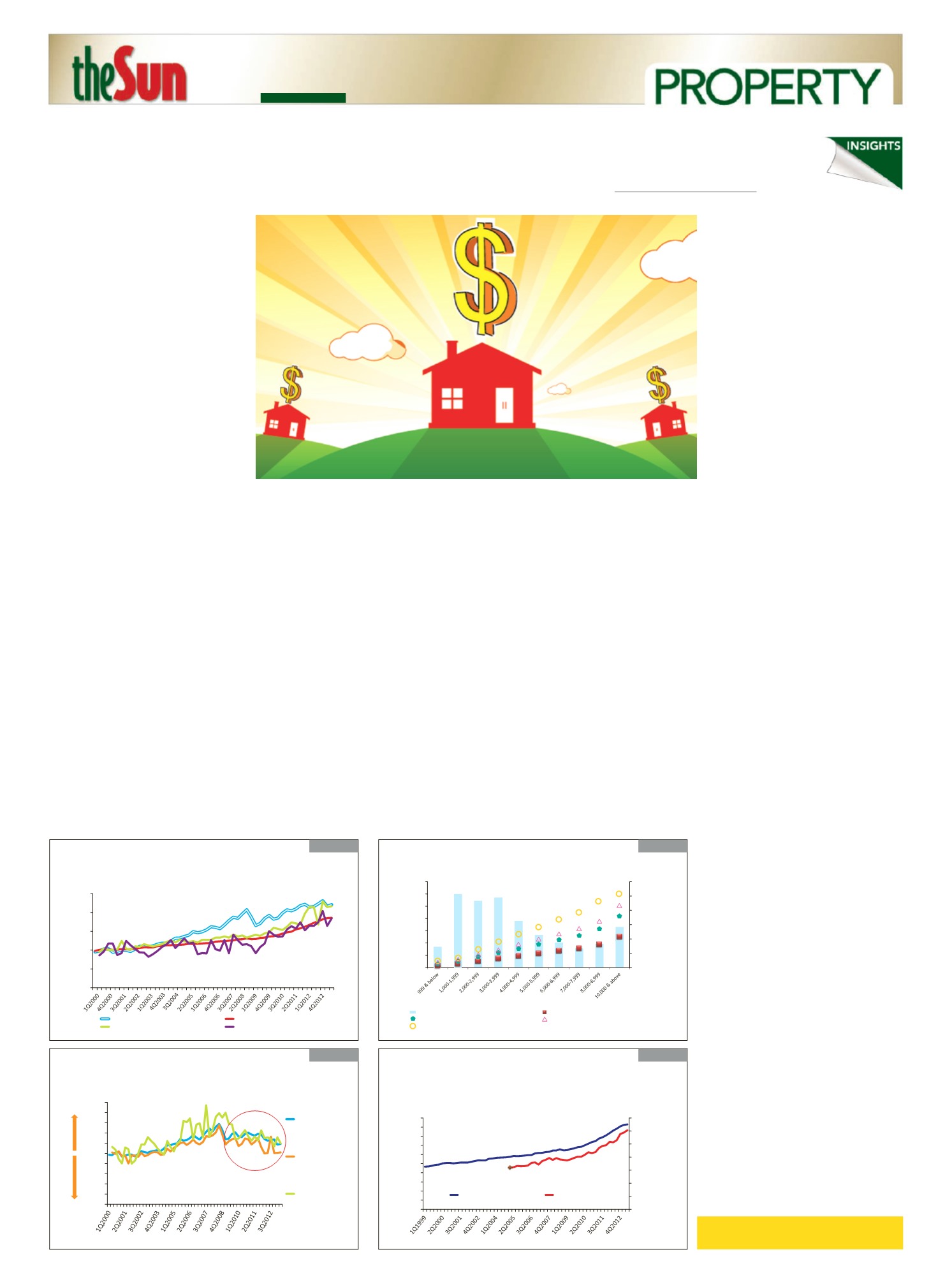

For a clearer picture, refer to the graphs

below taken froma research headed by Yeah

in 2012.

“Another index is calculated by assuming

that not more than half of the gross monthly

household income goes into repaying the loan

taken to buy the house. If there are a few

bread earners living in the same house who

contribute to the payment of the property,

then not more than 50%of their combined

income should go into paying the instalment/

rent of their house.” This index is useful to

provide a gauge on affordability by house

price and income segments,” explains Yeah.

POINTS INQUESTION

Yeah further shares about the issues

pertaining to housing affordability. He claims

there are

threemain issues

which are:

1) the rapid rise in house prices across all

segments;

2) insufficient supply tomeet demand; and

3) mis-match in the supply of affordable

homes.

“House prices have increased

tremendously, especially in the last five years.

Looking at house prices some 10 years or

more ago, there was a gradual increase of

Income and house price indexes

Source:NAPIC,CEIC

0

50

100

150

200

250

Index 2000=100

Income (GNI) per capita (2000=100)

HPI (2000=100)

KL: 1-1 1/2 Storey Terraced

KL: Condominium

House price increases have caught up with income increases

Affordability indexes

Source:NAPIC,CEIC

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

Income-to-HPI

raƟo

Income-to-KL

terrace house

price raƟo

Income-to-KL

condo price

raƟo

Rise

Fall

Steady decline in national-level affordability

about 3.2% in the prices every year. But

in the

last five years, the average annual

increase has risen to 9.7%

. At the rate

prices of houses are increasing, it is not

sustainable as the rate of income growth is

not rising as fast. And

if house prices

continue to spiral at the rate it is rising at,

the housingmarket will either face a soft

landing or amarket crash

, depending on

howhigh it peaks,” informs Yeah. The

positive outcome is that it will lead to

amore

gradual and sustainable rate of increase

in house pricing, one that is in linewith

the rise in income

.

Touching on point two, Yeah says,

“According to census figures published by the

Department of Statistics, there were 6.8

million households compared to the 4.8

million housing stock in 2012. Rental

properties made up 20%of the housing stock.

This means that the total number of

households that did not own a house summed

up to about 3.8million. We then subtract the

incoming supply of 0.73 million units, and the

planned supply of 0.62 million units, and

found there was still a housing shortage of 2.5

million homes.” Yeah then cited the 200,000

additional newhouseholds (based on yearly

estimated figures), concluding an estimated

shortfall of 2.7million housing units, still.

We deliberate the fact that house prices

within the KLmetropolitan city and Klang

Valley have sky-rocketed, somuch that it is

rare to find one within the city limits for less

than RM1 million. This leads to his third

point of which Yeah expounds, stating that

the

current housing supply in urban

areas are hugely beyond the reach of

the lowandmiddle income groups

.

“Research showed that 55%of the 6.8

million households have amonthly income

of less than RM4,000, which points to the

fact that this segment of society can only

afford houses priced around or below

RM360,000.” Interestingly yet

frighteningly, we arrive at many

implications on how just the

affordability

issues could slowly but surely affect

lifestyles, and eventually the socio-

economic health and political stability

of the country

. (See Graphs C andD)

ADDRESSING THE ISSUES

As it took years for such issues to crop up,

likewise, good foresight, the collaboration

of various industry-related players and

governing bodies, effectivemonitoring of

enforced rules and time, can bring positive

change. “

Monetary, fiscal and housing

policies need to be aligned, looked into

and perhaps fine-tuned to smoothen out

soaring house prices so it does not exceed

an average of 3% to 4%annually over

several years

. This can be achieved through

a combination of supply-side and demand-

sidemeasures,” Yeah recommends. On the

supply side, he adds that givenMalaysia’s

relatively lowpopulation density, the

challenge is

to increase supply of homes

that are priced to the pockets of the

masses

. “There is a need to cap expectations

and sentiments that house prices only go

north. But as seen in the recent property

market crash in the developed economies,

prices can fall 30-70%. On the demand-side,

rising house prices have ignited speculative

demand, especially for those who see

property investment as a hedge against

inflation,” he adds.

Yeah also raises the fact that we must be

aware that urban housing trends and lifestyle

changes need to cater to the ever-changing

demographic needs and patterns. He urges

the government to intervene, especially to

boost the chunk of the housing shortage

problem, which is to

accommodate those

in the lowandmiddle income segments

with affordable housing, especially in

urban areas

. For a start, he highlights some

areas that could be examined and further

explored, such as:

provision of adequate and cost-effective

basic amenities and transport

infrastructure;

release of state-owned land for housing;

establishment of public-private

partnerships in township developments;

promotion of industrialised building

systems (IBS); and

innovations in low- and medium-cost

building design, construction and

financing.

Still, although figures and charts may

determine one’s capability of owning a house,

there are other factors to bear inmind – the

list of additional expenses that come with

owning a house and running a home. These

include electricity, water and sewage bills,

not forgetting the twice-yearly property

assessment tax and annual quit rent. For

owners of high-rise units, there is the

management, maintenance and parking fees,

along with today’s internet, telephone and

cable or satellite TV charges, plus a longer list

of household and lifestyle expenses, which

are higher if one has a family to upkeep.

** Research and graphs are based on figures

taken fromaDepartment of Statistics survey

done in 2012.

X

X

X

X

X

Affordability by income groups

Source:HouseholdIncomeSurvey2012,DOSM;calculations byauthor

342

1,203

1,087

1,142

759

308

390

663

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

0

200

400

600

800

1,000

1,200

1,400

Affordable house

price (RM)

'000 households

Incomegroup(monthlyincome inRM)

EsƟmated number of households ('000)

Affordable price based on 3x annual income (RM)

Affordable price based on 5x annual income (RM)

Affordable price based on 6x income (RM)

Max house price based on loan eligibility (RM)

533

410

House price trend

Malaysia’s HPI and KL average price trends

Source: BIS; BNM

93.4

185.9

RM319,529

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

0

20

40

60

80

100

120

140

160

180

200

RM/dwelling

HPI

2000=100

HPI (naƟonal, 2000=100)

National

-

level House Price Index (HPI) rose 85.9% between 2000

and 2H2013, or a compound annual growth rate of 8.7% pa

GRAPHA

GRAPHB

GRAPHC

GRAPHD